Minimum Drawdowns for Account Based Pensions

1.

Introduction

Superannuation law requires that account based pensions paid from an SMSF must satisfy certain conditions. One of these conditions is that a minimum amount must be paid from the pension account each financial year.

2.

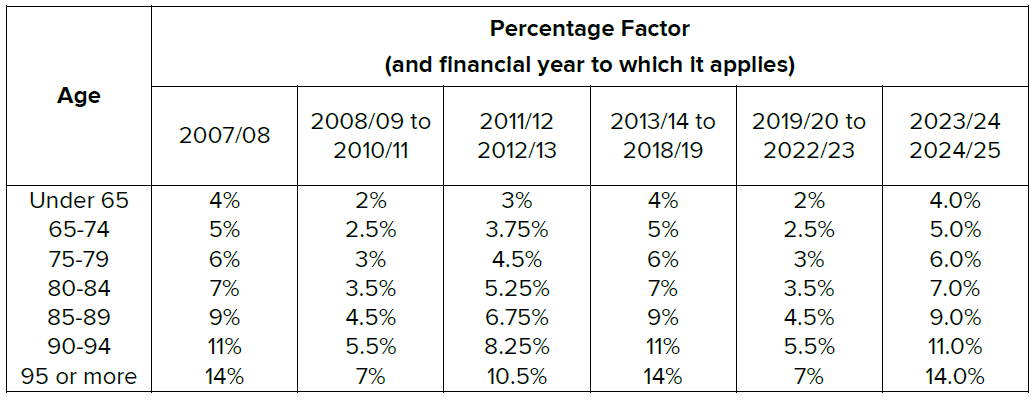

To calculate the minimum annual payment, the member’s pension account balance is multiplied by a percentage factor and then rounded to the nearest 10 dollars.

Minimum annual payment = percentage factor x account balance.

The percentage factors are shown in the table below:

The account balance used in this calculation will be either the member’s pension account

balance on 1 July in the financial year in which the payment is made, or if the pension

commenced during the financial year, the account balance on the commencement day. Similarly,

the age used is the member’s age on 1 July in the financial year in which the payment is made, or

if the pension commenced during the financial year, the member’s age on the commencement

day.

As can be seen in the above table, the minimum drawdown amounts for 2008/09, 2009/10 and

2010/11 were halved to provide relief from the decline in the investment markets arising from the

global financial crisis. This relief continued in 2011/12 and 2012/13 as a 25 percent reduction to

the usual percentage factors. The minimum drawdown amounts returned to normal for the

2013/14 to 2018/19 financial years. For the 2019/20 to 2022/23 financial years, the minimum

drawdown amounts have also been halved, to provide relief from the impact of COVID-19.

In the financial year in which the pension commences, the minimum is reduced to allow for the

number of days remaining in that financial year:

Minimum payment in first year = minimum annual payment x remaining number of days / 365 (or

366 in a leap year).

If the pension commences on or after 1 June in a financial year, no minimum payment is required

for that financial year.

3.

Account based pensions were introduced as part of the Simpler Superannuation reforms which

came into effect on 1 July 2007. The above standards for minimum pension drawdowns apply to

all account based pensions that commenced on or after 20 September 2007.

If your SMSF is paying a pension that commenced before 1 July 2007 it must continue to comply

with the previous pension payment standards unless the pension is an allocated pension. For

allocated pensions that commenced before 1 July 2007, you can elect to have the new minimum

standards apply without having to commute and start a new pension, provided your Fund’s trust

deed permits it. Alternatively, you can elect to continue to pay the pension under the previous

standards – which means the pension will have a different minimum and also a maximum

drawdown limit applying.

For SMSFs paying pensions that commenced between 1 July 2007 and 19 September 2007 you

can elect to either pay the pension under the previous or the new pension standards, provided

your Fund’s trust deed permits it.

Transition to retirement pensions commencing on or after 1 July 2007 also need to comply with

the above minimum pension drawdown standards. In addition to the minimum drawdown,

transition to retirement pensions have a maximum drawdown of 10% of the pension account

balance on 1 July of each financial year (or on the commencement day of the pension if it

commenced in that year).

If you are planning on fully commuting your

account based pension, you are still required to make the minimum drawdown for that financial

year before the pension is commuted. The minimum drawdown for the financial year in which

the pension is fully commuted is calculated on a proportional basis, in a similar way to when a

pension commences during the year.

If the pension is commuted due to the death of a member, no minimum payment is required in

that year. However, if the pension is automatically transferred to a dependent beneficiary as a

reversionary pension, the pension is continuing and so the minimum payment must still be made.

For the financial year in which this occurs, the minimum payment is calculated according to the

primary pensioner’s age. For the following financial year, the reversionary beneficiary’s age on 1

July must be used to calculate the minimum drawdown.

The information provided in this document is not financial product advice. It does not take into account your specific

circumstances or needs. While Verus SMSF Actuaries has taken care to ensure that the information is accurate

you should seek appropriate professional advice before acting on any of the information provided.

Updated November 2024